.png)

According to a Forrester study on global payroll, nearly half of enterprises plan to consolidate their payroll vendors within the next 12 months.

That number reflects a broader reality: most companies eventually outgrow their first payroll provider, whether because of pricing surprises, poor support, or a system that can't keep pace with a growing, increasingly distributed team.

Rise built its infrastructure with this transition in mind. Whether a company is moving off a legacy US payroll tool, consolidating multiple vendors into one platform, or adding global hiring capability for the first time, the switch doesn't have to mean months of disruption.

Rise supports domestic payroll through Direct Payroll, global employment through Employer of Record, and stablecoin-native payments through stablecoin payroll, all inside a single dashboard.

This guide covers when switching payroll providers makes sense, how to plan the migration without disrupting pay cycles, and what to evaluate in a new provider before you commit.

Key Takeaways

- Nearly half of enterprises plan to consolidate payroll vendors within 12 months, per Forrester.

- Rise's Direct Payroll runs US W-2 and 1099 payroll with a transparent $49/month minimum or $19 PEPM, whichever is greater.

- A structured 60-to-90-day timeline reduces the risk common to switching payroll providers.

- Rise unifies Direct Payroll, EOR, AOR, and stablecoin payments in one platform, avoiding future re-migrations.

Signs It's Time to Switch Payroll Providers

Most companies don't switch payroll providers on a whim. The decision usually surfaces after a pattern of friction becomes too costly to ignore.

The most common triggers include:

- Recurring payroll errors that damage employee trust or trigger compliance exposure

- Support response times that turn a routine payroll question into a delayed pay run

- Pricing structures that bundle unrelated fees or bury per-employee costs in tiered plans

- A provider that can't support global hiring once the team expands past domestic borders

- Manual workarounds because the platform doesn't integrate with existing HR or accounting tools

A single one of these issues might not justify a migration. Three or more, especially compounding around a growth stage, usually does.

Companies scaling from domestic to international hiring hit this wall often: the payroll tool that worked for 10 US employees can't handle a contractor in Portugal or a full-time hire in Singapore without adding a second vendor.

What Makes a Payroll Migration Risky

Payroll touches every employee, every pay period, and every tax filing deadline, which is exactly why the idea of switching feels riskier than it usually is. The actual risk concentrates in a few specific areas.

- Historical data transfer is the first: Year-to-date earnings, tax withholdings, and benefit deductions all need to carry over accurately, or year-end filings become a reconciliation project.

- Timing is the second: Switching mid-quarter means splitting W-2s or 1099s across two providers for the same tax year, which complicates both the employer's filings and the employee's personal tax return.

Communication is the third, and it's the one companies underestimate most. Employees need clear, advance notice about what changes (login credentials, pay stub formats, payout timing) and what doesn't (their actual pay date and amount). A payroll switch that surprises employees on payday erodes trust fast, even when the underlying system upgrade is a net positive.

Rise's onboarding process is built to compress this timeline. Employee data imports directly into the platform, tax profiles carry over cleanly, and Rise ID gives each worker a persistent identifier tied to their compliance and payment history, so a provider switch doesn't mean starting their record from zero.

The Right Timing for a Payroll Switch

The cleanest transition window is the start of a new calendar year or fiscal quarter. Making the switch at year-end means the outgoing provider closes out W-2s and 1099s cleanly, and the new provider starts with no split-year reporting to reconcile.

A quarterly switch is the next-best option when a January 1 transition isn't realistic. It still limits how much mid-year payroll history the new platform needs to carry forward, and it aligns cleanly with quarterly tax filings.

Companies with straightforward payroll structures, fewer than 20 employees on standard pay schedules with minimal benefit deductions, have more flexibility and can often switch mid-quarter without meaningful disruption. Complex, multi-entity, or multi-country payroll should build in more lead time, generally 60 to 90 days from decision to go-live.

What to Evaluate in a New Payroll Provider

Not every payroll platform solves the same problem. Before selecting a new provider, map the requirements that actually matter for the next stage of the business, not just the current one.

Consider these evaluation criteria:

- Domestic coverage: Does the platform calculate and file federal, state, and local taxes without manual workarounds?

- Global scalability: Can it support contractor and employee hiring abroad without forcing a second vendor?

- Pricing transparency: Are fees isolated by product, or do they bundle payroll costs with unrelated services?

- Integration depth: Does it sync with the accounting and HR tools already in use?

- Payout flexibility: Can workers choose how they get paid, including stablecoin or crypto options where relevant?

This is where many companies discover that switching payroll providers once, to the right platform, avoids switching again in 18 months when international hiring becomes a requirement.

Why Companies Choose Rise for the Switch

Rise's Direct Payroll handles US W-2 and 1099 payroll with automated federal, state, and local tax calculation, remittance, and filing. Pricing is billed on whichever is greater: a $49/month account minimum, triggered by any active employee, or $19 per employee per month.

That fee stays fully isolated from EOR or AOR costs. For a 3-person team, that's $57/month total, with no bundled add-ons and no surprise tiers.

What separates Rise from a US-only payroll switch is what sits behind Direct Payroll. The same platform runs Employer of Record for full-time hiring across 190+ countries, Agent of Record for contractor compliance, and stablecoin payroll that settles cross-border payments in minutes rather than the multi-day delays typical of SWIFT transfers.

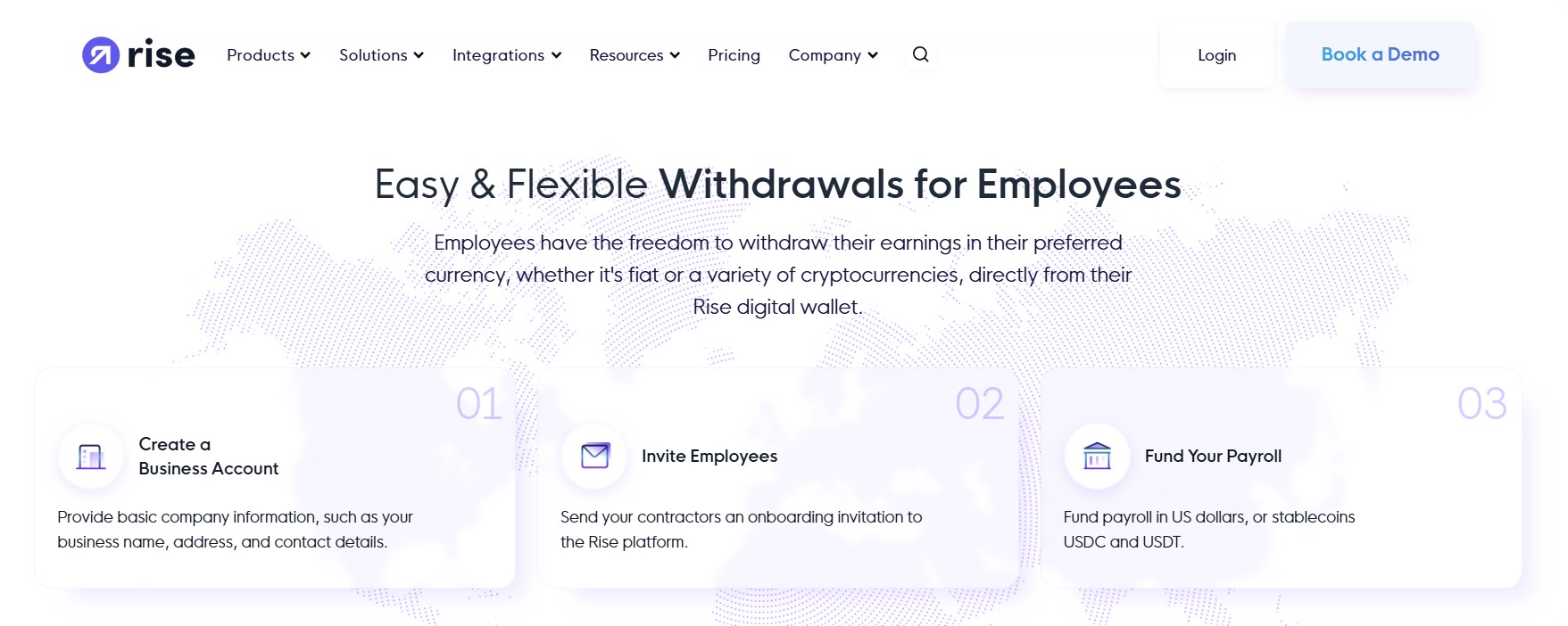

Rise's complete guide to crypto payroll breaks down how employers fund payroll in USD, USDC, or USDT while workers independently choose their withdrawal currency, fiat or crypto, without either side needing to coordinate on a single format. That flexibility matters most for companies that expect global hiring to be part of their next 12 months, not a future migration project.

Rise's compliance backbone includes SOC 2 Type II certification, FinCEN MSB registration, and GDPR compliance, so switching payroll providers doesn't mean trading operational simplicity for compliance risk.

Executing the Switch Without Disruption

A structured migration sequence keeps risk low regardless of company size.

- Start by auditing the current setup: employee count, pay frequency, active integrations, and any multi-entity structures.

- Next, request historical payroll data from the outgoing provider well before the contract ends, since data access often becomes harder after cancellation.

- Run a parallel test payroll cycle before full cutover, cross-checking amounts, deductions, and tax withholdings against the outgoing system.

- Finally, communicate the change to employees at least two full pay cycles in advance, covering what changes operationally and confirming that pay dates and amounts remain unaffected.

Switching Payroll Providers

Conclusion

Switching payroll providers carries real operational weight, but the risk sits almost entirely in poor planning, not in the switch itself.

A clear timeline, clean data transfer, and proactive employee communication turn a high-stakes migration into a routine operational update.

Rise's Direct Payroll, combined with global EOR and stablecoin infrastructure on the same platform, means the switch you make today doesn't need to be repeated when your hiring needs expand internationally.

Book a demo to map out your migration timeline with the Rise team.

FAQs:

1. How long does it take to switch payroll providers?

Switching payroll providers typically takes 60 to 90 days for companies with standard payroll structures, though simpler setups with fewer than 20 employees can move faster with proper planning.

2. What is the best time of year to switch payroll providers?

The best time to switch payroll providers is at the start of a new calendar year or fiscal quarter, since it avoids splitting W-2 or 1099 filings across two providers in the same tax year.

3. Does Rise's Direct Payroll handle both employees and contractors?

Rise's Direct Payroll is built for US W-2 and 1099 payroll, covering both employees and contractors with automated federal, state, and local tax filing under one transparent pricing structure.

4. Will switching payroll providers disrupt employee pay dates?

No. A properly planned migration, including a parallel test payroll cycle, ensures employee pay dates and amounts remain unaffected during the transition to a new provider.

5. Can Rise support global hiring if we're only switching US payroll right now?

Yes. Rise's Direct Payroll operates on the same platform as its Employer of Record and Agent of Record products, so global hiring can be added later without a second migration.

.png)

.png)

.png)